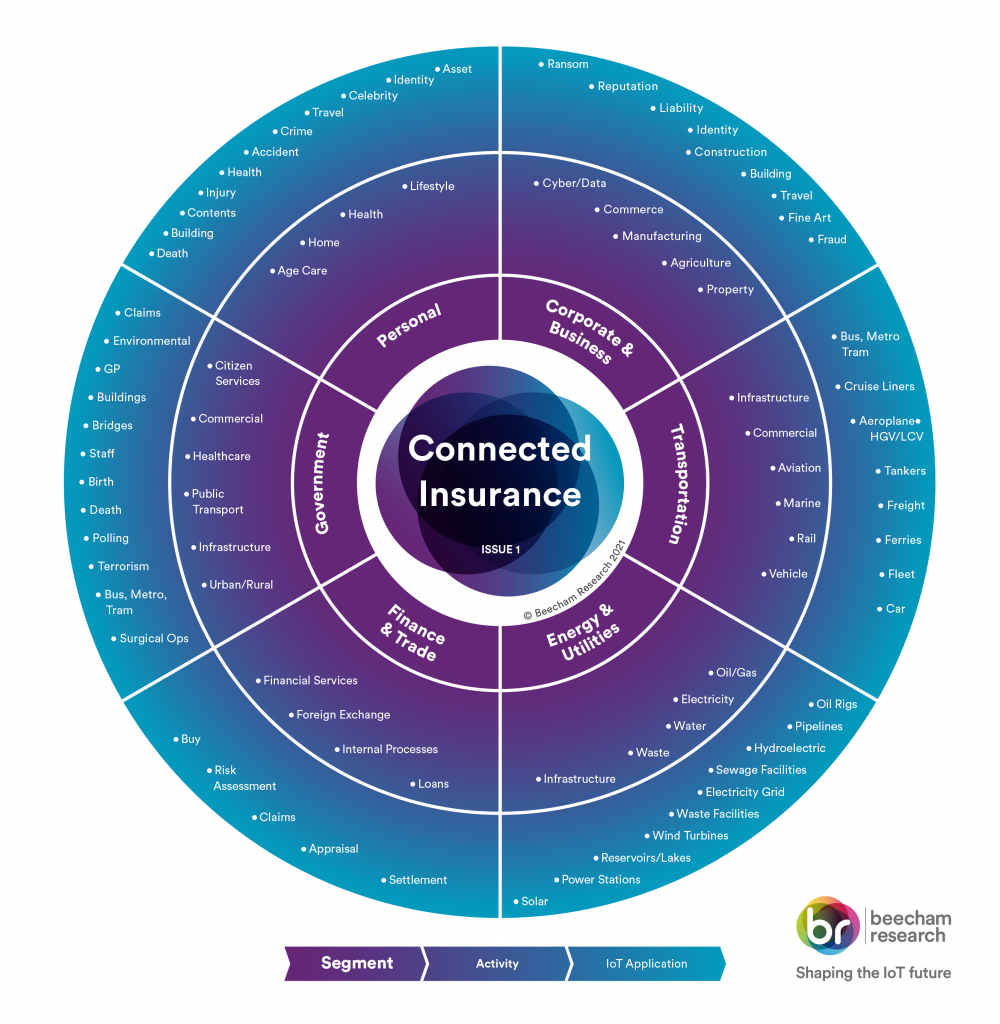

IoT in Insurance Overlay Chart

In this chart, the inner layer highlights the 6 key business segments of the insurance sector. The middle layer then indicates the types of activities those are in each of the segments. The outer layer then shows insurance policy areas associated with those types of activities where IoT may increasingly be involved. This is an overlay chart that draws on IoT applications across different IoT sectors.

Insurance is defined as the equitable transfer of the risk of a loss from one entity to another in exchange for a proportionate sum in payment. It is a form of risk management, used mainly to hedge against that risk; it enables the actuaries and insurance companies to judge the risk each subject bears, and to set their premiums accordingly. It also pools the risk across a diversified group.

In order to be able to insure a subject or object, a quantitative idea of the risk must be known. This can come from a wide range of information such as demographic, historic and other data. The advent of IoT now makes possible the collection of very large amounts of hitherto unobtainable data from a wide variety of sources. Clever analysis of sensor-related data will allow better understanding of the behaviour of a particular group of subjects or objects in great detail, so as to provide a more accurate calculation of risk than ever before. Such data may even be in real time or near real time, enabling a picture of a subject’s behaviour as it happens. As a result of this wider information base and faster analysis, insurers can assign scoring values to the data they collect, from which they can tailor their policies and premiums to better suit customer types, needs and behaviours to a higher level of granularity.

In addition to improved customer targeting, IoT also enables insurers to verify claims more rapidly and reliably.